Quant Research & Infrastructure.

Live-tested. Data-proven.

We design, validate, and operate systematic investment models — combining PhD-level research with engineering-grade infrastructure.

LIVE ML EQUITY STRATEGY — WARSAW STOCK EXCHANGE

Cumulative performance vs WIG20 benchmark (since Mar 2025)

Our Approach

Our research process combines financial intuition with engineering discipline. We treat each trading idea as a production system — measurable, reproducible, and continuously monitored. Every pipeline is versioned, backtested, and live-validated on the Warsaw Stock Exchange.

Data & Features

Daily and intraday GPW data, enriched with sector-level fundamentals, macro factors, and corporate events. Each dataset is versioned and reproducible.

Modeling Pipeline

Robust machine-learning pipelines built in Python and Rust, emphasizing walk-forward validation and cross-regime stability over raw backtest alpha.

Live Validation

Deployed models run live on the Warsaw Stock Exchange with automated reporting, Sharpe/Sortino tracking, and benchmark comparisons against WIG20.

We collaborate with funds, fintechs, and research institutions that demand verifiable results — not backtests. Our work focuses on building reproducible data infrastructure and live-tested trading systems that connect quantitative research with production reliability.

Expertise

We operate at the intersection of quantitative finance, software architecture, and applied machine learning. Each domain reinforces the other — from reproducible model validation to production-grade infrastructure.

Core Domains

Model Verification & Audit

Independent audits, leakage checks, and reproducible validation frameworks for academic and institutional research.

Portfolio Diagnostics

Automated Sharpe/Sortino dashboards, drawdown analytics, and institutional-grade tear sheets for transparent performance monitoring.

Machine Learning & Factor Research

Research and development of systematic investment models using machine learning, neural networks, reinforcement learning, and evolutionary optimization — with a focus on feature engineering, regime stability, and live model validation.

Infrastructure Engineering

Python, Rust, and Go pipelines — containerized, orchestrated, and continuously validated across research, backtest, and live production systems.

Built with Python, Rust, and Go — powered by containerized infrastructure and open-source ML frameworks.

Founders

We combine academic rigor with engineering execution — two founders, one goal: reliable, scalable, and data-proven systematic strategies.

Jeremi Kaczmarczyk

Engineer & System Architect

Builds and operates Silimare’s research infrastructure — reproducible data pipelines in Python and Rust, model orchestration, and automation for live systematic trading. Focuses on scalable backtesting frameworks, experiment management, and high-reliability systems that connect research with production-grade execution.

Klaudia Kaczmarczyk, PhD

Quantitative Research & Trading

PhD in Economics — specializes in machine learning for portfolio construction. Develops and validates systematic investment strategies through walk-forward testing, feature engineering, and portfolio optimization, focusing on live deployment for the Warsaw Stock Exchange (WSE).

Proof in Data

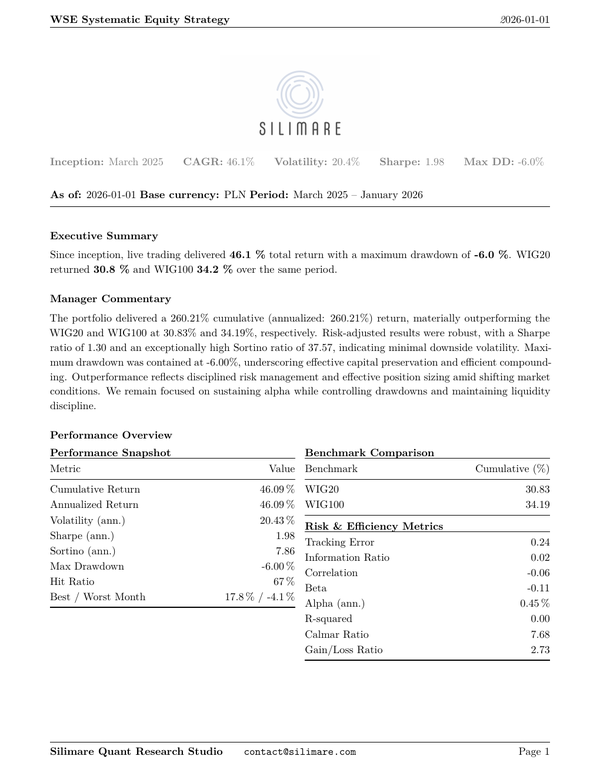

Verified monthly and independently benchmarked against WIG20 and WIG100. Each report is generated directly from live trading results and includes institutional-grade performance analytics.

Monthly Institutional Report

Latest report: January 2026 — Live WSE Equity Strategy

Preview shows first page. Download includes full institutional report.

Contact

Interested in collaboration, research exchange, or partnership? We’re open to selective engagements with funds, fintechs, and institutions.

Reach us directly via email or schedule a technical intro call.

contact@silimare.comBased in Wrocław, Poland · Working remotely